When I was in college I received more money than I needed my first year with student loans, scholarships and grants however I knew I was going to need the money in the coming years. So I was faced with a question, where should I stash my approximate $7.5k I was going to need within the next 1-3 years.

First I will tell you a little about my story and then 3 investing options for college students. Plus how a roommate in the same situation as me decided to gamble his extra money and he now makes his full time living off of it!

What Was My First Plan?

Initially I went on Morningstar.com and reviewed a bunch of mutual funds. My plan was to invest the money and hopefully make a 10% return (at least that is what I was thinking).

I had an older friend who was working on Wall Street so I figured he would be a good person to run my choices by, when I asked him he quite clearly said I was a fool to invest the money I needed for tuition in anything volatile. His rationale which makes sense to me is if the stock market tanks over the next year (a 1/10 chance – historically) I would have had struggled to find more student loans and likely ended up having to take a year off school to work.

This wouldn’t have been the end of the world but financially it would have meant 1 year working for pre-graduation wages vs 1 year working for post-graduation wages. This delay would have negatively impacted the financial return on my education.

What Did I End Up Doing With My $7.5k

In the end what ended up making the most sense for me and was recommended by my friend was to invest the money in a no-fee high interest, 2.75%, savings account from ING(Back in 2004 they actually had those).

3 Options If You Have Money to Invest but Will Need it In the Next 1-3 Years for College:

Option 1 – Low Risk – No Fee Savings Account

Currently ally has the highest interest for a savings account that includes…

- No minimum deposit

- No monthly maintenance fees

- 0.95% APY

The best comparison of savings accounts is from J.D. Roth from Get Rich Slowly on his page – High Yield Savings Account Comparisons

Another low risk option would be to invest in money market funds or CD’s. To learn more about these options you can read the comparison by Lisa White at fivecentnickel.com – Money Market or CD’s

“When choosing between a CD and money market account, it’s best to first determine your needs. Will this money be saved for short-term or long-term expenses? If you’re looking to use it for a vacation, car repairs, or a home expense within the next six months or less, a money market would be your best bet.

For rainy-day or more long-term savings, such as to cover expenses during a job loss or for a new house, a CD may be a better choice — especially if create a ladder of CDs with varying maturities such that you’ll have one coming due every 6-12 months.”

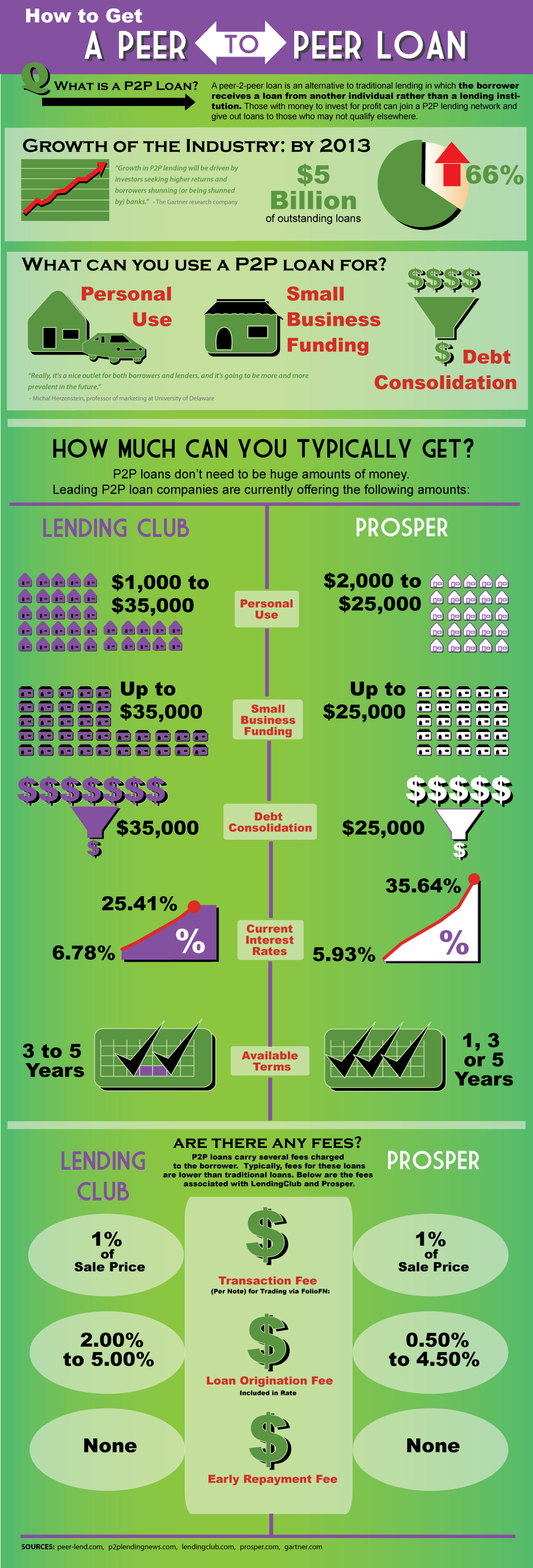

Option 2 –Medium Risk – Peer to Peer Lending

If you are less risk adverse a relatively new option exists that didn’t exist when I was faced with my question of what to do with extra money in college. That option is peer-peer lending, the returns and risks are higher.

Sam the Financial Samurai who is a very experienced investor wrote a review a couple months ago about why he was starting to invest in P2P lending specifically Prosper.com

“PEER-TO-PEER LENDING IS SAFER NOW

With regulatory oversight and now seven years of operating experience, I’m finally dipping my feet in the water. The advertised blended rate on Prosper.com is 10% and there have been no total blended losses for Prosper investors since 2009 who have at least 100 funded loans. 10% is currently over 5X the 10-year yield, which is also called the risk free rate. With my 3X risk-free rate bogie equaling 5%-6%, 10% is a very attractive proposition. The fact that Prosper investors showed positive returns even during the financial crisis is also very appealing.”

Source – Lendio

{kind=link}

Option 3 – Medium-High Risk – Invest In Individual Stocks

For such a short term investment I have to echo my friends advise (unedited) from several years ago…

”don’t be a dumb ass and risk a year of your education for the sake of potentially earning what… a couple hundred dollars, drink cheaper beer for the next few years and that will even itself out”

Friend when I was in college to me

How would I have done if I had invested instead of put my money into a savings account? I would have been up 8.8% on the year vs 2.75% in my savings account or $453.75 in lost opportunity. However, like he had said a 1/10 event was a couple years away and if the year had been 2008 I invested the money and wanted to take it out for the 2009/2010 tuition I would have been in trouble and likely had to take a year off.

If you are just getting started being interested in investing than a great option would be for you to read the Investing 101 series from Robert at The College Investor…

This is The College Investor, and these are a compilation of my best investing resources that I’ve put together for you for free! Investing is a powerful way to make your money work for you, but it comes with risks. Learn the basics, dive in, and see your money work for you instead of you just working for your money!

Are There Any Other Options?

Picture by rosswebsdale

Online Poker?!? – A housemate was in the same shoes as me and had a surplus of money year 1 and instead of investing it he started playing online poker. It actually worked out really well for him and he now plays professionally and makes a nice income.

If you are faced with this question of where to invest your money when you are in college I hope my story and these ideas will be of some help.

A simple and easily understood discussion about investing. Great information is provided. Thanks